The Medical Device Companies Building on Evidence, Not Just Innovation

The medical device industry has seen this pattern before. A transformative technology emerges. Early entrants race to market. Regulatory clearances multiply. And then the market discovers that clearance and adoption are not necessarily the same thing. The companies that survive the shakeout are rarely the ones that arrived first. They are the ones who have built clinical evidence that surgeons may require before changing their practice. In 3D-printed orthopedics, this shakeout is beginning. The winners may already be distinguishing themselves through evidence-based strategies that could define the market for years to come.

The regulatory pathway for additive-manufactured medical devices has matured significantly over the past five years. The FDA guidance for additive manufacturing established frameworks for evaluating 3D-printed implants that provided clarity to an industry previously navigating uncertainty. The guidance addressed material properties, manufacturing process validation, and device testing requirements specific to additive manufacturing. Companies that understood this pathway early gained time-to-market advantages. Those advantages are now likely diminishing as competitors catch up.

Additive Orthopaedics recognized that regulatory insight alone would not necessarily sustain a competitive position. The company has invested heavily in clinical evidence generation that goes beyond minimum regulatory requirements. Multi-center studies tracking patient outcomes, bone in-growth measurements, and long-term implant performance create a data asset that competitors may not simply purchase or replicate. The evidence takes years to accumulate. The competitive moat could deepen with each study completed.

The surgeon adoption dynamic makes this evidence strategy essential. Orthopedic surgeons are not typically early adopters by temperament or training. They have seen promising technologies fail. They have managed complications from devices that performed well in theory but poorly in practice. The burden of proof for changing surgical technique is substantial, and that burden is often discharged through clinical data, not marketing claims. The company that can present multi-year outcome data from hundreds of patients may have a conversation that companies with only regulatory clearance cannot access.

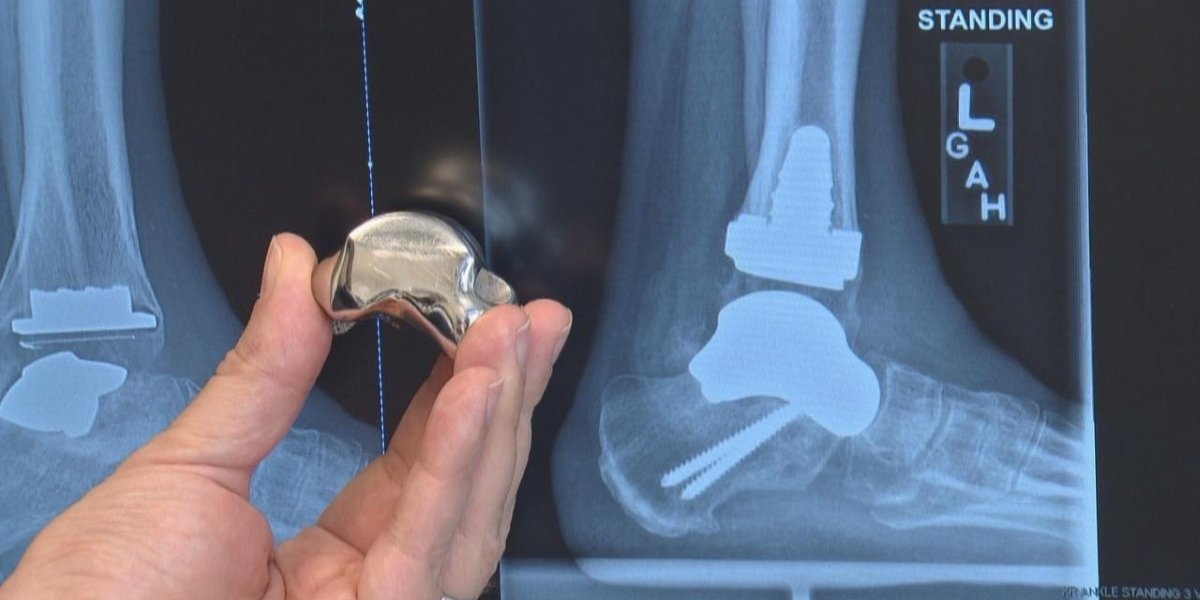

The clinical applications that Additive Orthopaedics has prioritized reflect a strategic focus on high-value, defensible positions. Total talus replacement addresses a condition with limited treatment alternatives, creating a clinical scenario where 3D-printed solutions may offer significant advantages over existing options. The acetabular revision system targets complex revision surgeries where standard components could fail, positioning the company in high-acuity procedures where surgeons have the greatest need for advanced solutions. Segmental bone reconstruction addresses defects beyond conventional repair capability. Each application represents a market segment where clinical evidence could create a sustainable advantage.

The technology platform enables applications, but evidence validates them. The research on lattice density and osseointegration demonstrates how Additive Orthopaedics approaches even technical design decisions with evidence generation in mind. The lattice structures that promote bone in-growth are not simply engineered. They are studied, measured, and documented. The data becomes ammunition for surgeon education, regulatory submissions, and competitive differentiation.

The Clinical Pulse signals commitment to transparency that could build trust with the surgical community. Ongoing publication of study updates, outcome metrics, and research progress creates visibility that surgeons may value. The company that shares data openly could earn credibility that proprietary approaches may not match. In a field where surgeons’ trust determines adoption, transparency is a strategy.

The surgeons portal reflects investment in the relationships that could drive market position. Providing surgeons with resources, case planning tools, and direct communication channels creates switching costs that could extend beyond product performance. The surgeon who has integrated Additive Orthopaedics into their workflow may have less incentive to evaluate alternatives. The platform becomes embedded in practice patterns.

The work process from imaging to implant delivery represents operational capability that evidence requirements demand. Patient-specific devices require reliable workflows that produce consistent quality across every case. The manufacturing and quality systems that deliver this consistency are themselves competitive assets, difficult for new entrants to replicate quickly or cheaply.

The 3D-printed orthopedics market could consolidate around companies that have built evidence foundations, while competitors focus on clearance alone. Regulatory approval opened the door. Clinical evidence may determine who walks through it with surgeon adoption waiting on the other side. Additive Orthopaedics has chosen the evidence path. The data accumulating today could determine market position for years to come.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute medical or professional advice. Readers should consult with qualified healthcare professionals or medical experts for guidance related to medical devices or treatments.