By: Jeremy Showe

When a direct-to-consumer (DTC) brand crosses the seven-figure mark, every tiny leak in the funnel starts to look like a burst pipe. Nowhere is that truer than at the checkout. Yet most teams still rely on the out-of-the-box flows that came with their stack—standard checkouts from ecommerce platforms or payment providers. Those defaults are great for getting live fast, but they were never engineered for the complexity of scaling. The result? Quiet, compounding losses that rarely show up in a headline KPI but drag on margins quarter after quarter.

Default Checkouts Were Built for Simplicity, Not Scale

Most default systems serve millions of small merchants, so their priority is ease of implementation. The trade-off is limited “under-the-hood” access:

- Single processor dependence. If your acquiring bank or payment rail hiccups, you have no automatic failover.

- Rigid, one-size-fits-all flow. You can tweak colors and a few fields, but you can’t fully A/B test layouts, offers, or payment sequences in real time.

- Minimal intelligence. Fraud rules, currency routing, and subscription logic sit a layer above the checkout, often in separate tools that don’t share data fast enough.

For a brand doing $20 million a year, even a one-percent dip in checkout conversion rate translates to six figures in lost revenue. But it’s not just the immediate sale that hurts—you also lose future rebills, upsell opportunities, and customer‐lifetime value.

The Four Hidden Costs No One Puts in the P&L

- Approval-Rate Leakage –Card-issuing banks use their own risk models. If you only run traffic through one processor, you inherit that processor’s decline profile. Industry research shows 5–15 % of legitimate transactions are declined on the first attempt. Without intelligent re-routing, those sales are gone forever.

- Failed Payment Recovery – Subscription brands rely on recurring billing. Default checkout tools treat failed rebills as an afterthought, leaving finance teams to chase delinquent accounts manually. A two-point improvement in failed payment recovery can lift monthly recurring revenue by tens of thousands.

- Lack of Real-Time Control & Testing – Growth leaders need the freedom to spin up an A/B test in an afternoon—new headline, different order bump, alternative wallet—without waiting on engineering sprints. Default systems force you into inflexible templates, so optimization ideas die in the backlog.

- Opportunity Cost of Siloed Data – Because processors, fraud tools, and upsell apps live in separate dashboards, ops teams can’t see a single source of truth. That slows decision-making and hides correlations (e.g., a spike in fraud declines after a new marketing campaign) that drive ecommerce revenue optimization.

Stripe vs Custom Checkout: When the “Good-Enough” Tax Kicks In

Many finance leaders calculate payment processing as a flat 2.9 % + 30¢ and move on. But the real math is more nuanced. Consider a brand with 100,000 monthly attempts at a $75 average order value:

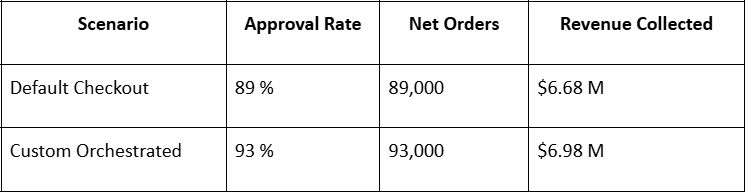

That four-point delta equals $300,000 per month—a “tax” paid for the convenience of staying default.

Enter Lasso: Checkout Built Like a Power Tool, Not an Accessory

Lasso was engineered specifically for high-volume DTC operators who need granular control without rebuilding the wheel.

- Multi-Processor Routing – Connect multiple gateways and let Lasso’s engine send each transaction to the processor with the highest likelihood of approval (or lowest cost) for that card type or geography. If the first path fails, the system retries on a backup in milliseconds—often saving the sale.

- Real-Time Split Testing – Growth teams can launch variations of copy, design, or payment sequencing with a toggle—no code deploys. Winners automatically scale, closing the feedback loop between idea and impact.

- Built-In Upsell & AOV Boosters – Post-purchase one-click upsells, intelligent cross-sells, and dynamic discounts are native features, not Franken-apps bolted on later. That means no extra latency and clean reporting.

- Unified Analytics & Subscription Management

Lasso stitches gateway responses, fraud signals, and CRM data into a single dashboard, so ops and finance teams see authorizations, declines, and rebills in one view. - Fraud & Compliance by Default

Global 3-D Secure, address verification, and velocity rules ship out of the box—without throttling conversion for good customers.

What Winning Brands Are Doing

Top DTC names now treat checkout the way SaaS giants treat their onboarding flow—as a revenue operating system. They:

- Run continuous checkout conversion rate experiments just like ad creative tests.

- Maintain at least three processors to diversify risk.

- Measure lifetime value impact of tiny changes (a 0.5 % lift in approvals multiplied over 12-month retention).

- Feed customer-level payment data back into marketing automation to personalize offers.

Those moves used to require a full-stack dev team. With Lasso, they’re mostly settings you toggle on.

Making the Switch Without Burning Dev Cycles

Migrating off a default setup doesn’t mean ripping out your entire stack. Lasso can sit on top of Shopify or any headless storefront via lightweight APIs and JavaScript snippets. Teams typically go live in weeks, not quarters, because:

- Product and growth set up routing rules in a visual editor.

- Finance maps processors to the best interchange rates.

- Developers focus on edge cases instead of core payments logic.

The ROI shows up fast: higher approval rates, recovered rebills, and richer data for the next optimization cycle.

The Bottom Line

Sticking with default checkout flows is like driving a sports car locked in second gear—it works, but you’re leaving speed on the table. For brands chasing aggressive growth targets or eyeing healthier EBITDA multiples, those hidden costs compound quickly.

Whether you call it Stripe vs custom checkout analysis or a broader ecommerce revenue optimization audit, the message is the same: once you’re processing at scale, “good enough” is anything but.

If you’re ready to plug the leaks and turn checkout into a profit center, explore what a purpose-built platform like Lasso Checkout can do. Your finance dashboard—and your customers—will thank you.

Disclaimer: The information provided in this article is for general informational purposes only. Readers are encouraged to conduct their own research before making business or technology decisions.